Artificial intelligence might seem like magic, but even magic needs rules. One of the biggest misconceptions about AI is that it always gets things right. In reality, AI is only as useful as the data it works with. And when you’re managing complex asset catalogs across thousands of projects, bad data can snowball into real-world delays, rework, and costly mistakes.

At Ephany, we’re focused on managing the kind of data most project teams overlook: fixtures, furniture, and equipment (FF&E). These assets may seem small, but when you’re working across hundreds or thousands of locations, tracking the right assets (with the right options and finishes) is a massive job. This is where our agentic AI steps in… Not just to automate data extraction, but to double-check its own work.

Garbage In, Headaches Out: The Real Cost of Bad Asset Data

Imagine you’re rolling out a new store design, and the same refrigerator model is listed three different ways in your system. One record is missing dimensions, another was typed in twice, and a third doesn’t list which finish is required. That might not seem like a big deal, but do you really want to wait until the wrong asset gets ordered, it shows up late, or your drawings don’t match what’s on site?

In a traditional workflow, someone on the project team would have to comb through spreadsheets or drawings to find these issues. It’s tedious, it’s slow, and it’s prone to human error.

Every day a new store or facility opening is delayed means lost income. Retail industry analyses estimate that major retailers lose about $1.1 million in sales per day for a delayed store opening. Even a small-format restaurant can lose roughly $7,000 in revenue per day it cannot open. These losses add up quickly, and they come on top of rising capital costs – construction costs themselves climb an estimated 5% for each month a project is postponed. (source)

Meet the AI That Calls Out the Mess Before It Spreads

Ephany uses agentic AI with autonomous agents that do more than just extract data. They actively validate it.

When a new asset is added to the catalog, or when data is pulled from PDFs, Revit models, or scanned documents, Ephany’s AI agents perform automated checks in real time.

They flag:

Inconsistencies (e.g., mismatched descriptions, dimensions, or part numbers)

Duplicates (multiple entries of the same asset under different IDs)

Missing fields (required metadata like finishes, power requirements, or vendor details)

Instead of waiting for someone to catch these errors manually, the AI catches them before the asset is provided to the design team, purchased by the procurement team, or installed by the construction team.

Why It Matters

Validation checks might not sound exciting, but they’re the backbone of reliable asset management. They keep your data clean, your procurement teams confident, and your construction timelines intact. They also make your AI smarter over time. Every validation step helps train the system to get better at spotting what doesn’t belong.

Ephany is Leading the Way

While many platforms use AI as a buzzword, Ephany is building real-world solutions using agentic AI to improve asset data where it matters most. We believe automation should come with accountability—and that’s why our validation checks are built in from the start.

Your asset data should work as hard as you do. With Ephany, it finally can.

Despite the continued growth of e-commerce, physical retail in the U.S. — particularly in the big-box and grocery sectors — remains remarkably resilient.

From 2022 to 2023, store openings outpaced closures. In 2022, retailers opened approximately 5,400 stores and closed 3,800, resulting in a net gain of 1,600 locations (source). In 2023, the gap narrowed slightly, with 5,800 openings and 5,500 closures — still a net positive (source).

By 2024, the trend reversed. Rising costs, economic pressure, and a wave of bankruptcies led to over 7,300 store closure announcements — up nearly 60% year-over-year (source). However, these closures were largely concentrated among struggling specialty retailers and legacy chains, not grocery stores or big-box operators like Walmart or Costco, which have remained stable or expanded.

Importantly, physical stores still handle the majority of retail sales. In 2023 about 72.6% of U.S. retail sales occurred in stores (approx. $3.72 trillion of $5.13 trillion total), with roughly 27.4% online (Online returns outpace in-store in 2023, NRF report finds). Categories like groceries remain predominantly in-store – online grocery sales were only around $95 billion in 2023 (under 10% of total grocery expenditures). Consumer preferences reveal that while convenience of e-commerce is valued, shoppers continue to gravitate to stores for immediacy, product discovery, and experience – especially for food and essential goods. By late 2024, improving consumer sentiment led to higher-income shoppers increasing visits to big-box and specialty stores (e.g. for furniture, apparel), not just to discounters (Retailers Saw More Foot Traffic Last Year. But What Does That Say About 2025?). In sum, foot traffic recovered to near or above pre-pandemic levels in many segments (grocery foot traffic in Q3 2024 was 12% higher than 2019 baseline (Retail 2024 Wrap and 7 Trends in Store for 2025 | LightBox)) – a testament to brick-and-mortar’s enduring role. Strong in-store holiday sales growth in 2024 (+2.7% YoY) alongside a 6.7% online rise shows the channels growing in tandem, with physical retail holding its own (Retail 2024 Wrap and 7 Trends in Store for 2025 | LightBox).

Crucially, retailers have adapted to new shopping habits by blending online and offline experiences. Shoppers increasingly use omnichannel options – e.g. buy-online-pickup-in-store (BOPIS), curbside pickup, and in-store returns for online orders – driving incremental foot traffic as well as online sales. Chains report that physical stores act as fulfillment hubs for e-commerce: Target, for example, fulfills the vast majority of its digital orders from stores, and offers services like Drive Up curbside pickup at all locations (New Target Stores and Facilities) (New Target Stores and Facilities). This integration of e-commerce with physical locations has further cemented stores as a critical touchpoint in the customer journey, boosting store productivity and keeping foot traffic robust by catering to consumers’ desire for speed and flexibility in how they receive goods.

Key Developments at Major Retailers (Big-Box & Grocery)

Many leading big-box and grocery chains pursued targeted expansion and strategic store portfolio changes from 2022 to 2025, rather than wholesale contraction. Below are key developments for major players:

Starting in late 2023 and into 2024, Walmart shifted back to expansion mode. The retailer announced plans in January 2024 to open 150+ new stores in the U.S. over the next five years (Walmart | All items Wiki | Fandom) – an average of ~30 stores per year through 2028. Most of these will be large-format Supercenters that align with its omnichannel strategy (ample space for a full assortment and for staging online orders) (Walmart Shrunk by 100+ Stores Last Year — a Smart Move for What’s Next – Business Insider). In fact, adding just one new 150,000 sq. ft. supercenter offsets the square footage Walmart shed by closing dozens of small formats (Walmart Shrunk by 100+ Stores Last Year — a Smart Move for What’s Next – Business Insider). Walmart is also heavily remodeling and “refreshing” existing stores: 650 locations are being upgraded to its new “store of the future” concept with improved layouts, technology, and expanded pickup/delivery areas (Walmart Shrunk by 100+ Stores Last Year — a Smart Move for What’s Next – Business Insider). These modernized stores better serve as e-commerce fulfillment hubs and enhance the in-store experience with improved merchandising and integration of Walmart’s app for navigation and checkout (Walmart Shrunk by 100+ Stores Last Year — a Smart Move for What’s Next – Business Insider). In parallel, Walmart’s warehouse club division (Sam’s Club), buoyed by record membership, announced plans in 2023 to open ~30 new Sam’s Club warehouses over the next few years (after a five-year hiatus in new club openings). Overall, Walmart’s strategy indicates renewed investment in physical retail: closing underperformers and smaller concepts while expanding big boxes and enhancing omnichannel capabilities in-store.

Target

Target has been in an expansionary mode, growing its store count with new formats while addressing challenges in select locations. The company added 21 new stores in 2023 (and 23 new stores in 2022) across a mix of urban hubs, suburbs, and college towns (New Target Stores and Facilities). These include a combination of large-format Targets (approx. 125,000–150,000 sq. ft.) and small-format stores in dense city neighborhoods. In 2023 alone Target opened a dozen new large stores (including a ~135,000 sq. ft. prototype in Texas) and nine small-format stores in locations like downtown Brooklyn and near Auburn University (New Target Stores and Facilities) (New Target Stores and Facilities). This multi-size approach lets Target “flex to fit” different communities – from a <20,000 sq. ft. college campus store to a multi-story urban store (New Target Stores and Facilities). The chain has nearly 2,000 stores nationwide (approaching that milestone by end of 2024) (New Target Stores and Facilities), and it plans to keep growing: Target has stated ambitions to open ~30 new stores per year (approximately 300 over the next decade) (Investing in Target Stores), which would push its store count well beyond 2,000.

At the same time, Target confronted some headwinds in certain locations. In 2023 the company closed at least 13 stores, primarily small-format urban stores opened in the last five years that did not meet performance goals (Target’s store closures seem to highlight challenges of small-format model ). Notably, Target announced in late 2023 the closure of 9 stores across four cities (including NYC, San Francisco, Seattle) citing concerns over theft and organized retail crime affecting profitability (Target’s store closures seem to highlight challenges of small-format model ). These closures – mostly in dense urban areas – sparked debate about whether the small-store urban model faces economic challenges (shrink, lower volume) despite Target’s success overall (Target’s store closures seem to highlight challenges of small-format model ). Company officials noted that shrink (inventory loss) had risen, but only marginally (0.2% increase in shrink rate) (Target’s store closures seem to highlight challenges of small-format model ), suggesting crime was a factor but not the sole driver. Retail analysts believe a combination of factors (higher costs, lower sales volumes, and shrink) made certain city stores unsustainable (Target’s store closures seem to highlight challenges of small-format model ). Nevertheless, these closures were a tiny fraction of Target’s fleet. The net result: Target still added more stores than it closed in 2023, and it continues to invest heavily in physical retail. Over 160 existing Targets were remodeled in 2023 (New Target Stores and Facilities), adding features like larger Order Pickup/Drive Up areas, modernized decor, expanded grocery sections, and new in-store brand partnerships (e.g. Ulta Beauty shop-in-shops in 140 more stores) (New Target Stores and Facilities). Target’s stores-as-hub strategy – using stores to fulfill online orders and as convenient pickup points – is central to its growth (New Target Stores and Facilities). In summary, Target is expanding its footprint (particularly in urban and suburban trade areas not previously served) and upgrading stores, while making surgical closures where needed. Its strategy emphasizes omnichannel service, smaller formats for new markets, and experiential enhancements to keep shoppers coming in.

Costco’s performance underscores why it’s doubling down on stores: foot traffic and membership metrics are very robust. Wholesale clubs saw some of the retail sector’s strongest visit growth – in 2024, visits to Costco stores were up ~7.2% year-over-year (Placer.ai: Wholesale clubs see visits rise to start 2025). Even during a tough economy, Costco achieved 8.9% YoY traffic growth in early 2023 (Costco bucks trend: Surge in foot traffic despite tough economy), as consumers were drawn to its value proposition (bulk savings amid inflation) (Costco bucks trend: Surge in foot traffic despite tough economy). Membership fee income – a key profit driver – rose 8% in late 2023 (Costco Plans to Open 31 New Locations in 2024 – Business Insider), indicating shoppers are flocking to join or renew. Costco has also been resistant to e-commerce displacement. While it offers online ordering for certain categories, the vast majority of Costco’s ~$242 billion in annual sales still flow through its cavernous stores, where the treasure-hunt atmosphere and in-person experience (think sampling and the famed $1.50 hot dog) remain a big draw. In the face of rising e-commerce, Costco and its peers (Sam’s Club, BJ’s) have proven that large-format value stores can thrive. All three major club chains are in expansion mode as of 2024 (Placer.ai: Wholesale clubs see visits rise to start 2025). Sam’s Club, for example, saw 4.8% visit growth in 2024 and has new units under development, and BJ’s Wholesale has entered new states with several new clubs each year. In summary, Costco’s strategy is expansionary: it is adding dozens of new warehouses through 2025, banking on the strength of its physical retail model. The overall warehouse club segment is booming, leveraging physical stores as their primary (and highly productive) channel.

Kroger (and Grocery Supermarkets)

Kroger Co., the nation’s largest traditional supermarket operator, took a slightly different tack – focusing on selective growth and a major merger rather than rapid organic expansion. As of early 2024, Kroger (which operates regional banners like Kroger, Ralphs, Harris Teeter, Fry’s, etc.) had about 2,722 grocery stores in 35 states (Number of stores operated by Kroger 2024, by category – Statista). This store base has been relatively stable: Kroger has neither dramatically expanded nor contracted its store count in the past few years. Instead, it has concentrated on incremental projects (new stores in high-growth areas, store enlargements, and relocations of older stores) and on an impending acquisition of rival Albertsons Companies. In 2023, Kroger opened, relocated, or expanded about 30 stores (net new stores plus replacements) (Kroger CEO talks merger, store expansion on earnings call) – a modest addition relative to its size. It has also invested heavily in store remodels and technology rather than opening hundreds of new locations. For example, many Kroger stores added space for pickup orders, and Kroger built automated fulfillment centers (in partnership with Ocado) to serve online grocery orders in regions where it has no stores (a “delivery-only” expansion model). This cautious expansion approach reflects that the grocery market is mature in many regions, and growth often comes via acquisition or e-commerce rather than brand-new supermarkets.

The headline development for Kroger is its proposed $24.6 billion merger with Albertsons (owner of Safeway, Shaw’s, Vons, etc.), announced in late 2022. If approved, this merger would create a grocery behemoth with nearly 5,000 stores nationwide (Kroger CEO talks merger, store expansion on earnings call). Throughout 2023–2024, Kroger has been navigating regulatory hurdles for this deal (the FTC sued to block it in late 2023) (Kroger CEO talks merger, store expansion on earnings call). To appease regulators, the companies drafted plans to divest 400–600 stores to other operators (e.g., selling hundreds of stores to C&S Wholesale Grocers) so that the combined entity wouldn’t dominate local markets (Kroger, Albertsons Companies and C&S Wholesale Grocers, LLC …). The outcome, expected in 2024 or 2025, could reshape physical grocery footprints: some overlap stores might change ownership or eventually close if buyers aren’t found. Kroger’s CEO, however, affirmed that with or without the merger, Kroger will continue opening stores and investing in its business (Kroger CEO talks merger, store expansion on earnings call). In 2024, Kroger remains “optimistic” and even without Albertsons, it plans to accelerate new store openings in coming years to drive growth (Kroger CEO talks merger, store expansion on earnings call). Beyond store count, Kroger has driven omnichannel integration – it offers delivery (including through its own services and third-parties like Instacart), pickup at over 2,250 stores, and has rolled out enhancements like smart shopping apps and customer analytics to sharpen inventory. Like many grocers, Kroger benefited from the pandemic-era shift to eating at home and elevated grocery demand, but it’s now contending with food inflation pressures and competition from Walmart, Costco, and Aldi. This has spurred Kroger to double down on its strengths: a wide store network (often in suburban neighborhoods), a strong private label program, and investments in efficiency (automation) and digital loyalty to keep customers coming in-store. In essence, Kroger’s physical footprint strategy is one of quality over quantity – maintaining a solid base of ~2,700 stores, selectively adding in key markets, and aiming to become a national powerhouse via the Albertsons merger.

Other Notable Chains: Discounters and Emerging Players

Outside the above giants, several other big-box and grocery-adjacent chains had significant impact on physical retail trends:

Dollar Stores (Dollar General, Dollar Tree/Family Dollar) – The small-format discounters have been the most prolific store openers in recent years. Dollar General surpassed 20,000 U.S. stores in 2023 (Dollar General store count by state U.S. 2024 – Statista), after opening roughly 1,000 new stores annually (mainly in rural and small-town markets). Similarly, Dollar Tree Inc. (which owns Family Dollar) has been adding hundreds of stores each year. These chains’ ultra-convenient locations and low-price merchandise drew heavy foot traffic during high-inflation periods. Placer.ai data showed discount & dollar store visits up ~11% in Q2 2024, outpacing most retail sectors (6 Retail Real Estate-Shaping Trends That Stood Out in Q2, Plus Retail CMBS and Consumer Resilience | ICSC). Dollar General and Family Dollar did announce some isolated store closures (e.g. Family Dollar closing ~400 stores in 2024 as it rationalizes its footprint) (Coresight Research: More retail store closings than openings so far in 2024 – REJournals), but these were far outweighed by new openings. Going forward, dollar stores are aiming to diversify offerings (adding more grocery, fresh produce in some locations) to capture even more share from supermarkets. However, they also face margin pressures and saturation in certain areas, which has led Dollar General to slightly scale back its breakneck opening pace to about 800 new stores planned in 2025 (Dollar General Plans 575 New Stores, 4,250 Remodels, Tests Same …). Still, this sector remains a major contributor to net physical store growth in the U.S., especially in underserved rural communities.

Costco’s Competitors – Aside from Costco, Sam’s Club (Walmart-owned) and BJ’s Wholesale Club expanded physical operations. Sam’s Club, riding a ~ membership surge, announced in January 2023 it would open about 30 new clubs over the next few years – its first major expansion in a decade. BJ’s opened 11 new clubs in 2022 and continued adding new locations in 2023, entering new states like Tennessee and its 20th state (Missouri) (Placer.ai: Wholesale clubs see visits rise to start 2025). All three warehouse clubs are thus growing their store counts, reflecting the strength of the bulk-buying format post-pandemic.

Aldi and Lidl (Discount Grocers) – Aldi, the German no-frills grocer, has aggressively grown its U.S. store base. By 2024 Aldi operated over 2,400 stores in the US (Aldi plans more than 220 new store openings for 2025) and is on a path to reach 2,500+ by 2025. It opened nearly 120 stores in 2024 alone (Aldi opened nearly 120 stores in 2024 – Supermarket News), and announced plans for 225 more store openings in 2025 as part of a five-year growth strategy (Aldi plans to open 225+ new stores in 2025 – Produce Blue Book). In mid-2023, Aldi made a bold move by acquiring 400 stores of Winn-Dixie and Harveys (regional grocery chains in the Southeast), which will either be converted to the Aldi format or operated under those banners, significantly expanding Aldi’s footprint in the southern U.S. Aldi’s emphasis on low prices and small, quick-to-shop stores has attracted millions of new customers (19 million new shoppers in 2024 per the company). Its fellow European discounter Lidl also grew to around 200 U.S. stores, though at a slower pace and with a few closures of early locations. The discount grocery segment is thus expanding physically, capitalizing on consumers’ hunt for grocery savings.

Best Buy and Home Improvement Chains – Not all big-box formats expanded; some more mature sectors saw stable or slightly contracting footprints. For instance, Best Buy (big-box electronics) has been slowly reducing its number of stores (often by not renewing leases on older stores) as more electronics sales move online; Best Buy closed a couple dozen stores in 2022–2023, focusing on e-commerce and smaller concept stores. Home Depot and Lowe’s, the home improvement giants, generally held their ~2,000+ store counts steady, opening only a handful of new stores (Home Depot opened just 3 new U.S. stores in 2022 and a few more in 2023) – instead investing in supply chain and distribution centers. These categories illustrate a trend of optimization over expansion in sectors where online competition is strong or the market is saturated.

Amazon’s Physical Retail Experiments – E-commerce leader Amazon also influenced physical retail trends by opening – and in some cases closing – stores. Amazon’s acquisition of Whole Foods (500+ stores) made it a major grocery player; Whole Foods opened some new locations in 2022–2024 and remodeled many for Amazon integration, but growth has been moderate. Amazon also launched Amazon Fresh grocery stores and Amazon Go convenience stores in several cities. After a rapid rollout, Amazon paused new Fresh store openings in 2022 to retool the concept, and in early 2023 it closed some Amazon Go stores in cities like San Francisco and NYC, citing performance issues. While Amazon remains committed to physical grocery (it restarted opening Fresh stores in 2023 and is testing a new upscale Fresh design in 2024), the mixed results showed that even for Amazon, brick-and-mortar retail has a learning curve. This underscores that physical retail expansion is being concentrated in proven formats (like big-box discount and grocery) rather than experimental concepts.

Trends Driving Shifts in Physical Retail

Multiple industry-wide trends have driven the expansion or contraction decisions of big-box and grocery chains in 2022–2025:

Post-Pandemic Recovery & “Revenge Shopping”: After 2020’s lockdowns, consumers eagerly returned to stores in 2021–2022. Retailers enjoyed a post-pandemic sales boom aided by stimulus-fueled savings (NRF | Store closing announcements up, along with retail bankruptcies). This lifted physical store performance, encouraging chains to resume new store projects put on hold in 2020. By 2022, mall traffic and shopping center occupancy had largely bounced back. Strong demand and low vacancy (shopping center vacancy hit a 20-year low of 5.3% (6 Retail Real Estate-Shaping Trends That Stood Out in Q2, Plus Retail CMBS and Consumer Resilience | ICSC)) emboldened retailers to expand. This momentum explains why store openings outpaced closures in 2022–23 (‼️Closing Up… – Bliss Realty & Investments Commercial | Facebook). However, as stimulus effects waned and pent-up demand normalized, retailers in 2023 faced a tougher environment with shifting spending patterns (goods back to services) and depleted excess savings (NRF | Store closing announcements up, along with retail bankruptcies). The post-pandemic high gave way to more normal consumer behavior by 2024, requiring retailers to refocus on fundamentals and efficiency rather than just riding a rising tide.

Omnichannel Integration: The past three years have solidified the omnichannel model – blending e-commerce with stores – as the dominant retail strategy. Major chains invested in making physical stores integral to their digital operations. This includes BOPIS (Buy Online, Pickup In Store) and curbside pickup services at almost every big-box and grocery store, dedicated in-store pickup counters or drive-up lanes, and using store backrooms as micro-fulfillment centers for online orders. Target, for example, attributes much of its e-commerce success to its stores: nearly all Target’s online orders are fulfilled by a local store (for either pickup or home delivery) (New Target Stores and Facilities). Walmart expanded its curbside pickup nationwide and added automated pickup towers and local delivery from stores. The result is that stores have evolved into hybrid retail/fulfillment hubs, boosting their economic viability. Retailers also integrated digital apps in the in-store experience (for wayfinding, self-checkout scans, digital coupons), creating a seamless journey. This omnichannel emphasis has driven physical expansions in distribution-friendly locations (e.g., adding backroom space or new stores in areas to improve delivery coverage). It also means store performance is now measured by more than foot traffic alone – a store that sees heavy pickup volume or ships out lots of online orders is extremely valuable, even if traditional walk-in traffic is lower. Overall, the blending of channels has reinforced the importance of having a dense store network close to customers, supporting the expansion plans of Walmart, Target, Aldi, and others.

Value and Inflationary Pressures:High inflation from 2022 into 2023 (especially food inflation) had a dual impact: it squeezed consumers’ wallets, but it also increased nominal sales for grocery and discount retailers. Consumers responded by seeking value – shopping more at Walmart, dollar stores, warehouse clubs, and discount grocers. This drove those retailers to expand to capture demand. Placer.ai noted that early 2024 visits were elevated at value-focused chains like Dollar General and Five Below as cost-conscious behavior prevailed (Retailers Saw More Foot Traffic Last Year. But What Does That Say About 2025?). Club stores saw membership growth as families looked to buy in bulk and save (Costco bucks trend: Surge in foot traffic despite tough economy). At the same time, mid-tier and luxury retailers felt more pressure as discretionary spending tightened. The net effect was expansion in the value segment (Dollar General, Aldi, Costco all opened many stores) and selective closure in higher-priced formats (e.g. department stores continued to close some locations). Inflation also pushed operational costs up (labor, rent, utilities), which hurt marginal stores’ profitability. Some retailers preemptively closed a handful of underperforming stores to cut costs – for example, Walmart cited profit underperformance when closing a couple dozen stores in 2023 (Walmart Shrunk by 100+ Stores Last Year — a Smart Move for What’s Next – Business Insider). In summary, inflationary times reinforced a “flight to value” among shoppers, benefiting big-box discounters and grocers and influencing where retailers invested in new stores (e.g. Aldi accelerating openings) versus where they pulled back.

Urban vs. Suburban Strategies: Retailers have been recalibrating where to grow. There’s been a notable urban push by some, and a retreat by others. Target’s expansion into city centers with small-format stores was a defining strategy of the last decade (Target’s store closures seem to highlight challenges of small-format model ), filling a gap left as other big boxes (and grocery chains) focused on suburban locations. However, as seen in 2023, these urban stores can face unique challenges (higher rents, different shopping patterns, crime issues) (Target’s store closures seem to highlight challenges of small-format model ) (Target’s store closures seem to highlight challenges of small-format model ). Target’s closure of certain city stores in 2023 highlights that urban expansion must be executed carefully – site selection and store economics are critical. Meanwhile, Walmart generally stayed out of small urban box formats after a failed attempt years ago, and instead is now focusing on large suburban supercenters and rural stores, where it excels. The ICSC reported that even traditionally large-format chains are “slimming down” prototypes to fit into compact urban spaces when needed, using a “smaller-yet-smarter” model to maintain profitability (6 Retail Real Estate-Shaping Trends That Stood Out in Q2, Plus Retail CMBS and Consumer Resilience | ICSC). On the flip side, many retailers doubled down on suburban growth, as suburban migration ticked up post-pandemic. Grocers like Publix, H-E-B, and Kroger opened stores in growing suburbs and Sunbelt regions to chase population shifts. Mixed results in urban experiments (e.g., some of Target’s small stores underperforming) mean we may see a tempered approach: urban stores will still open, but with refined formats and expectations, while suburban expansion (often in communities seeing housing growth) remains robust. Additionally, retailers are eyeing “food deserts” and underserved areas for expansion – Dollar General and Aldi, for instance, strategically open stores in rural or inner-city neighborhoods with few fresh food options, both to drive sales and to meet community needs.

Labor and Operational Challenges: The retail labor market was extraordinarily tight in 2021–2022, which led to labor shortages and rising wage costs. Many stores cut operating hours or struggled to hire, which could delay new store openings. Big chains responded by raising starting wages (Target set a $15 minimum, Walmart followed with $14–17 range, etc.) and investing in automation (self-checkout kiosks, electronic shelf labels, backroom robotics) to alleviate labor pressures. By 2023, labor shortages had somewhat eased, but retailers still face higher labor expense. This has made store productivity more crucial – stores that can’t justify labor costs may close. It’s also driven some automation of store tasks (for example, Walmart is rolling out robotic inventory scanners and automated fulfillment systems in many stores). Labor unions and strikes emerged as a factor too: grocers on the West Coast dealt with union negotiations that could affect labor costs and store operations. Additionally, supply chain disruptions and inventory glut in 2022 forced retailers to optimize their store inventory and in some cases use stores as overflow warehouses. All these operational challenges have nudged retailers to be more cautious in expansion (fewer speculative new stores) and more focused on efficient formats that require less staffing. However, the industry’s recent moves – e.g. Walmart’s plan for 150 new stores – show that these challenges, while considered, are not deterring strategic growth.

Retail Crime and Store Safety: An unfortunate trend impacting physical retail is the rise of organized retail crime (ORC) and theft (shrinkage). Many retailers cited increasing shrink in 2022–2023, which pressured margins. High-profile closures (like some Walgreens, and the aforementioned Target stores) were partially attributed to theft making those locations unprofitable (Target’s store closures seem to highlight challenges of small-format model ). The NRF reported shrink hit $94.5 billion industry-wide in 2021 and grew further in 2022, although as a percentage of sales the increases were small (Target’s store closures seem to highlight challenges of small-format model ). Still, retailers have responded with enhanced security measures, and in a few cases, store closures in crime-plagued areas to ensure employee and customer safety. While this issue affects a minority of stores, it’s a factor in urban markets especially. It has not led to widespread retreat from cities, but we see companies lobbying for stronger theft prevention and considering shrink as a factor in site selection. If crime issues persist, retailers might favor opening stores in areas with lower risk or investing more in security (which increases operating costs). This trend underscores that store viability isn’t just about sales – it’s also about controllable losses and environment.

Real Estate and Formats: Retail real estate conditions have influenced store strategy. With record-high occupancy rates in open-air shopping centers (92% at end of 2023) (Vacancy Isn’t a Bad Word Anymore, 2024 Store Plans for 5 Retailers …), landlords have fewer vacancies, and retailers looking to expand may find limited prime space. New retail construction has been very low (only ~50 million sq. ft. under construction in Q2 2024, near historic lows) (6 Retail Real Estate-Shaping Trends That Stood Out in Q2, Plus Retail CMBS and Consumer Resilience | ICSC), meaning retailers often must refit second-generation spaces or pay premium rents for new builds. This has led to creative solutions: many chains opt for smaller footprints or locate in mixed-use developments. The ICSC notes that spaces under 2,500 sq. ft. were leased fastest, often by food and service tenants (6 Retail Real Estate-Shaping Trends That Stood Out in Q2, Plus Retail CMBS and Consumer Resilience | ICSC), but even large retailers are taking slightly smaller store formats to squeeze into high-demand locations (6 Retail Real Estate-Shaping Trends That Stood Out in Q2, Plus Retail CMBS and Consumer Resilience | ICSC). Additionally, drive-thru and curbside capabilities have influenced store format – retailers want sites where they can have dedicated pickup parking or drive-thru lanes (important for grocery and mass merchant click-and-collect). In response, some big-box retailers are even testing new concepts: e.g., Walmart is experimenting with a convenience-store-sized format attached to gas stations; Kroger is piloting “Kroger Pickup Only” spots without full stores in certain areas; and Kohl’s is leasing out parts of its stores to grocery partners (Aldi in some Kohl’s) to utilize space. The overarching trend is a strategic reconfiguration of store formats – right-sizing stores for each market and maximizing the utility of each square foot (often to accommodate omnichannel services).

Outlook: The Future of Physical Retail in Big-Box & Grocery

Looking ahead, experts anticipate a resilient but evolving future for physical retail in the big-box and grocery sectors. While economic headwinds (and an expected uptick in closures in 2025) will pose challenges, major retailers are planning long-term investments in stores rather than retreating.

Store Count Forecasts: Industry analysts project that retail store openings will slow somewhat in the near term, but continue in sectors like grocery, discount, and convenience. 2025 may see around 5,800 new store openings in the U.S., slightly fewer than 2024, while store closures could reach 12,000–15,000 as some struggling chains shutter locations (Hugh Suhr on LinkedIn: Twice As Many Stores In The U.S. Are …). This implies a net decline in total stores for the first time in years, driven largely by consolidation (e.g. merger-related divestitures) and bankruptcies of weaker retailers. However, the closures are expected to be concentrated in underperforming brands and saturated categories (e.g. pharmacy chains, department stores, specialty apparel), rather than in grocery or big-box discount. In fact, big-box retailers and grocers are generally expected to grow their revenue and store bases modestly in 2025, leveraging their strength in value and essentials. S&P Global forecasts big-box retailers to grow revenues ~3–7% in 2025 and continue to perform well as consumers seek value and one-stop convenience ([PDF] Industry Credit Outlook 2025 – Retail and Restaurants – S&P Global).

Continued Expansion by Leaders: Top chains have signaled they will open more stores and enter new markets. For instance, Costco plans ~30 warehouses per year globally going forward (Costco Plans to Open 31 New Locations in 2024 – Business Insider) (with ~15 in the U.S. annually), a pace that if sustained would put it near 650 U.S. stores by 2028. Walmart’s 150 new U.S. stores plan (over 5 years) (Walmart | All items Wiki | Fandom) means it will extend its reach, likely focusing on high-growth regions and replacing older stores in its network. Target is aiming for 2,500+ stores by end of the decade (adding 30 per year with a mix of formats) (Investing in Target Stores), bringing its urban-mini and larger store concepts to many new neighborhoods. Aldi’s five-year plan calls for 120+ new stores per year, which will push it toward 3,000 US stores by 2028 (Aldi opened nearly 120 stores in 2024 – Supermarket News). Even dollar stores, though slightly moderating growth, each still plan hundreds of new units in 2025 (Dollar General ~575 openings; Dollar Tree, a similar scale) (Dollar General Plans 575 New Stores, 4,250 Remodels, Tests Same …). On the flip side, we expect more pruning of underperforming locations by certain chains – e.g. CVS and Walgreens are closing hundreds of drugstores through 2024–25 as they pivot strategy, and regional grocers involved in mergers will shed overlapping stores. The net effect likely sees physical grocery and big-box store counts holding steady or rising slightly over the next few years, while some other retail channels contract.

Strategic Shifts: Physical retailers will increasingly focus on quality of experience and efficiency in each store. Many chains are embracing technology to enhance in-store shopping – for example, retailers are expected to roll out more personalized digital features and experiential elements to draw shoppers in. Analysts predict that in 2025 retailers will “focus on personalized in-store experiences and technology to boost foot traffic and engagement.” (4 more retail predictions for 2025) This could mean more in-store events, product demos, local community ties, or services like personal styling and cooking classes offered for free to entice visits (4 more retail predictions for 2025). We also anticipate further omnichannel innovation: stores will get smarter about handling online orders (with automated pickup lockers, drive-thru pickup windows, etc.), and retailers will use data to ensure the store and digital channels complement each other. Store formats will keep evolving – expect to see more small-format stores from big players (as they target urban cores and campus locations) alongside new large flagship stores in booming suburbs. The success of hybrids like Target’s multi-sized approach suggests others (perhaps Walmart or grocers like Kroger) could experiment again with smaller formats or pop-up locations to extend reach. Additionally, experiential flagships will be key for some brands: e.g., Costco is even planning its largest store ever (241,000 sq. ft. in California) (Costco Plans to Open 31 New Locations in 2024 – Business Insider) to serve as a mega-destination, and grocers are adding food hall sections, breweries, or cooking schools in select stores to enhance appeal.

Integration of AI and Automation: By 2025–2026, technology will further entwine with physical retail. From AI-driven shelf stocking and checkout-free technology to advanced customer analytics guiding store layouts, retailers will leverage tech to improve margins and the shopper experience. Amazon’s influence will be felt as it brings its Alexa AI (codenamed “Project Rufus”) into physical stores to assist customers (4 more retail predictions for 2025). Robotics and AI may help mitigate labor issues and keep stores running smoothly (we might see more robotic cleaners, automated fulfillment in backrooms, and maybe a resurgence of cashierless checkout experiments as tech matures). These innovations are aimed at making stores more efficient and engaging, which in turn supports keeping stores open and profitable.

Resilience of Brick-and-Mortar: Perhaps the clearest forecast from experts is that physical retail will remain indispensable in the big-box and grocery sectors. Jack Kleinhenz, chief economist of NRF, noted in late 2024 that despite challenges, consumer resilience and economic growth prospects are positive, and the U.S. consumer will remain a “dominant narrative” in 2025 (Retailers Saw More Foot Traffic Last Year. But What Does That Say About 2025?) – implying continued robust retail spending that will flow largely through stores. Retailers with strong value propositions and omnichannel execution are expected to prosper. The physical store is also becoming key to last-mile logistics; we anticipate more retailers using their store networks as bases for super-fast delivery (1-hour delivery from store, etc.), blurring the line between retail store and distribution center. In addition, many brands that started online (direct-to-consumer brands) are continuing to open brick-and-mortar shops or partner with big boxes for shelf space – a trend that should sustain demand for retail real estate. Mall operators and shopping center owners are repurposing vacant spaces with grocery anchors, discount retailers, and non-retail uses to keep centers vibrant, which could reduce the doom-and-gloom of empty storefronts.

In conclusion, the overall direction for big-box and grocery physical retail is cautiously expansionary. The footprint of stores is expected to grow in segments like grocery, mass merchandise, clubs, and discount – albeit at a moderate pace – while contracting in over-stored segments like traditional department stores and pharmacies. The years 2024–2025 are a period of shakeout and refinement: retailers are closing weaker locations and doubling down on high-performing formats and regions. Physical retail’s role has undeniably shifted (with omnichannel and experience now paramount), but it remains the cornerstone of how Americans shop for everyday goods. As a result, top retailers are not only keeping stores open but actively investing in new ones and revamping old ones. The store counts of Walmart, Target, Costco, Kroger, and their peers in 2025 and beyond will likely be higher than today, and those stores will be more technologically advanced and integrated than ever. Analysts describe the current trend as “the store strikes back” – a recognition that brick-and-mortar retail has proven its resilience and will continue adapting to serve customers in an omnichannel world, rather than disappearing.

Summary Table – Major Chains: Store Count Trends & Strategies (2022–2025)

– New formats: Launching small-format urban stores (typically 12k–40k sq ft) to penetrate cities and campuses, while also rolling out larger-format 135k+ sq ft stores with extended assortment (New Target Stores and Facilities). – Remodeling push: Remodelled 160+ stores in 2023 (New Target Stores and Facilities); adding Disney, Ulta Beauty shop-in-shops and enhanced grocery sections to existing stores. – Stores-as-hub strategy: Utilizing stores for 95%+ of online order fulfillment (Drive Up, Order Pickup) (New Target Stores and Facilities), investing in backroom space and technology to facilitate fast omnichannel fulfillment. – Urban expansion & recalibration: Grew aggressively into dense markets (100th NYC-area store opened in 2023) (New Target Stores and Facilities), but now refining small-store model after some closures (addressing shrink and sales mix issues in urban locations) (Target’s store closures seem to highlight challenges of small-format model ).

– Warehouse club growth: Ramping up to ~30 new warehouses per year globally (about half in U.S.) to broaden membership base (Costco Plans to Open 31 New Locations in 2024 – Business Insider). – High traffic & loyalty: Capitalizing on record membership renewal rates and strong foot traffic (+7.2% visits in 2024) (Placer.ai: Wholesale clubs see visits rise to start 2025) – doubling down on the treasure-hunt in-store experience (e.g. sampling, food court). – Global expansion: Entering new international markets (e.g. first stores in New Zealand, Sweden) while infilling U.S. markets with demand (e.g. new stores in urban California and New Jersey). – Measured omnichannel: Increasing online offerings and delivery options (Instacart, same-day) but keeping stores as primary sales channel; testing self-checkout and mobile checkout to improve in-warehouse experience.

Stable with slight growth. Opened or relocated ~20–30 stores per year (net change small). Preparing for major jump in store count pending Albertsons merger (would roughly double total). Some overlapping stores may be divested if merger approved.

– Merger & consolidation: Pursuing acquisition of Albertsons Cos. to reach ~5,000 stores (Kroger CEO talks merger, store expansion on earnings call); planning to divest hundreds of overlapping stores to other operators to satisfy regulators (Kroger, Albertsons Companies and C&S Wholesale Grocers, LLC …). – Incremental growth: Continuing to build a limited number of new supermarkets in growing markets and replacing older stores with larger, modern ones (Marketplace format). – Digital and delivery focus: Investing in Ocado-powered automated fulfillment centers for online orders, and expanding curbside pickup and delivery to nearly all stores (to defend market share against Walmart/Amazon). – Efficiency & margin initiatives: Closing a few underperforming stores when necessary, enhancing supply chain, and expanding private-label offerings to keep prices competitive amid inflation.

Rapid expansion. Approximately 1,000 new stores opened annually (2022–2023), pushing store count from ~17,000 (2020) to 20,000+ by 2024. Plans ~900+ new stores in 2024–2025. A few dozen older stores closed or relocated (minimal relative to openings).

– Ubiquity strategy: Aggressively opening stores in rural and small-town America, aiming to be within 5 miles of most U.S. households. Focus on low-cost buildouts and quick profitability. – Adding produce & fresh: Testing expanded coolers and fresh produce in hundreds of stores to capture grocery spend; launching DG Market larger-format stores in some areas. – Economic resilience: Benefiting from trade-down effect as consumers seek bargains ([6 Retail Real Estate-Shaping Trends That Stood Out in Q2, Plus Retail CMBS and Consumer Resilience

Expansion and acquisition. Opened ~120 new stores in 2023 ([6 Retail Real Estate-Shaping Trends That Stood Out in Q2, Plus Retail CMBS and Consumer Resilience

Experimentation and recalibration. Whole Foods store count up modestly (opened a few new flagship stores in 2022–23). Amazon Fresh (launched 2020) expanded to ~40 stores by 2022, then paused new openings in 2023 and closed a few underperformers. Amazon Go cashierless stores peaked ~30, with several closures in 2023 as concept was retooled.

– Whole Foods optimization: Upgrading stores with Amazon tech (palm-pay, app checkout) and integrating online ordering (Prime delivery) but keeping growth modest. Exploring smaller Whole Foods “market” concepts in suburbs. – Amazon Fresh reboot: After pausing expansion to revisit the format (assortment and technology), Amazon in 2024 resumed opening Fresh stores with a refined concept (greater fresh food focus, improved checkout tech). – Cashierless tech: Amazon Go’s future being reassessed – some closed in high-cost urban areas; Amazon may apply the Just Walk Out tech in larger store formats (e.g., airport stores, Whole Foods sections). – Physical presence: Amazon sees stores as crucial for grocery and as pickup/return hubs for online orders – likely to continue investing in grocery stores (organically or via acquisition) to expand its physical retail footprint, albeit at a cautious pace.

Building out physical retail stores is a high-stakes game—one where a single misstep can cost thousands (or even millions). Have you ever had a store opening delayed because the wrong fixtures arrived? Or watched in horror as a brand-new display case was installed upside down? You’re not alone. Mistakes in procurement, installation, and project management can quickly turn a well-planned rollout into a financial nightmare. The good news? These costly issues are avoidable.

In this article, we’ll break down the biggest money pits in retail construction—inefficient procurement, supply chain mishaps, installation blunders, and budget overruns—and, more importantly, how to prevent them. Read on to find out how better planning, smart project management, and a little foresight can keep your FF&E costs under control and your store openings on schedule.

1. Inefficient Procurement Processes

Disorganized or ad-hoc procurement of FF&E can lead to higher prices, inconsistent quality, and delays. Lack of centralized purchasing and poor vendor management mean retailers miss out on bulk discounts and reliable delivery schedules.

Centralized procurement can improve efficiency by up to 30% in multi-location operations, and long-term vendor partnerships can cut costs by ~20% through negotiated pricing (source).

Retailers without these strategies often face overbudget spending and late deliveries. For example, not standardizing FF&E specs or consolidating orders across stores can result in variability in pricing and quality, as well as rush orders that incur premium shipping fees.

Reduce Procurement Inefficiencies in Three Ways

StandardizeFF&E for designs across projects (ensures consistency and bulk leverage).

Centralize procurement and negotiate volume deals with vetted vendors (captures economies of scale and better terms).

Leverage technology for procurement – e.g. ERP or procurement platforms – to track orders and budgets. Digital procurement tools have been shown to reduce costs by ~10% while improving transparency (source).

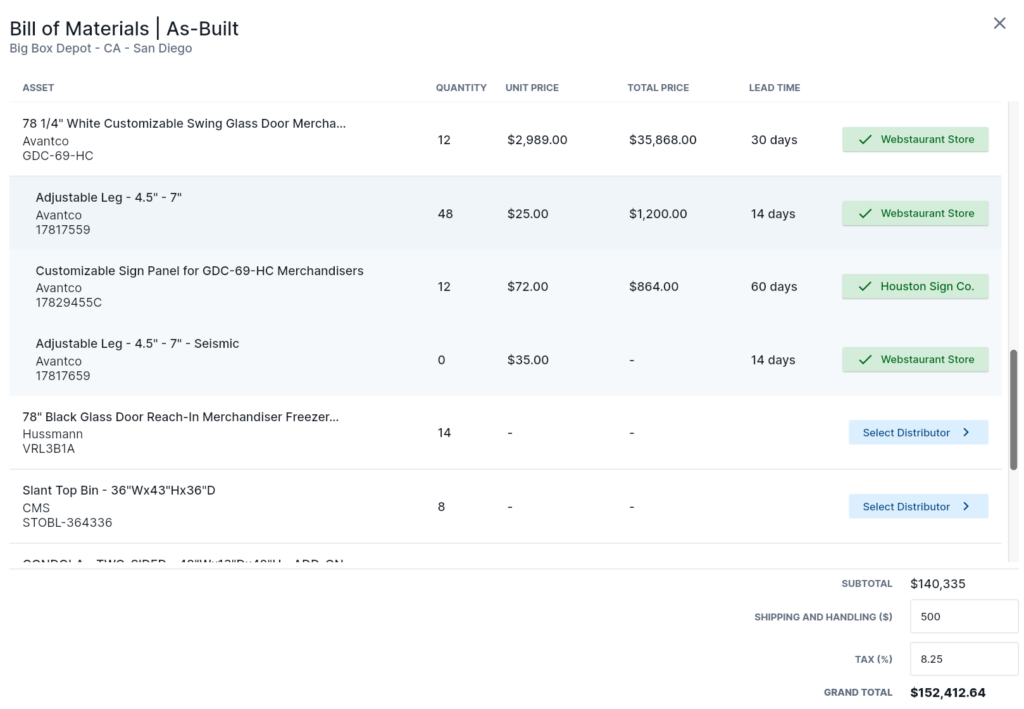

Ephany streamlines the way your team manages FF&E procurement by giving you complete visibility into assets, their components, and sourcing details—all in one place. Instead of scrambling to track fixture parts, distributor options, pricing variations, and shifting lead times across spreadsheets, Ephany centralizes this data, ensuring your team always has accurate and up-to-date information. With the ability to generate a detailed bill of materials (BOM) in just a few clicks, you get a clear, real-time picture of costs and availability, helping you make informed decisions, prevent budget overruns, and keep projects on schedule.

Creating a bill of materials (BOM) based on assets from in a Revit model in Ephany.

2. Installation Errors

Poor workmanship or rushed installation of fixtures and equipment can trigger costly rework and repairs. Mistakes like misaligned shelving, improper electrical hookup of equipment, or installing items in the wrong sequence can damage assets and require do-overs.

Studies show that construction rework (i.e., redoing work due to errors or changes) typically eats up about 5–9% of a project’s cost (source). In the U.S. alone, rework accounted for an estimated $65 billion (5% of total construction spending) in 2020 (source).

Best Practices to Avoid Installation Errors and Rework

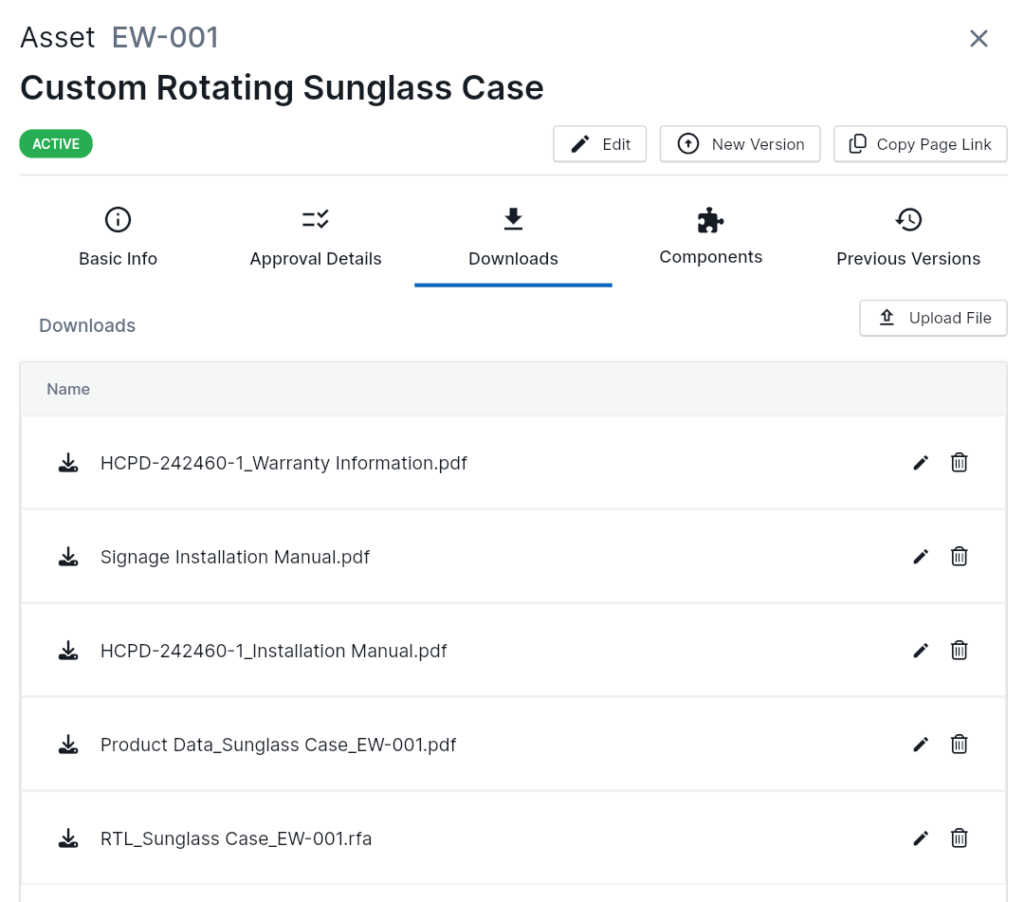

Clear, accessible documentation is essential for ensuring FF&E installations are done right the first time. Without the right specifications and guidelines, contractors risk costly mistakes, delays, and rework. Investing in document control not only streamlines installation but also helps maintain consistency across multiple locations.

Ephany makes this effortless by providing a centralized hub for all FF&E documentation. Teams can store and organize PDFs, CAD files (DWG), and BIM models—including Revit families—directly within the asset catalog. This ensures that contractors and project teams always have the latest, most accurate information at their fingertips, reducing errors and keeping installations on track. No more hunting through emails or outdated files—just seamless access to the data you need, exactly when you need it.

Managing supporting documentation for FF&E (assets) in Ephany.

3. Supply Chain Disruptions

Global supply chain issues can wreak havoc on retail construction projects. Volatile material costs and long lead times for FF&E have been a major driver of cost overruns and delays in recent years. For example, construction input costs surged ~17% in 2022 (far above general inflation), with core materials like steel up 124% and lumber up 61% since 2020 (source).

One national retailer saw its average per-store buildout cost jump from $400–500k to $700k due to these rising prices. Such increases at 40–75% per store forced that company to pause expansion to redesign for cheaper materials – an illustration of how supply-chain-driven cost spikes directly hit the bottom line.

Beyond cost, delayed shipments of critical FF&E can postpone store openings (leading to lost sales opportunities).

In a 2022 industry survey, up to 25% of material deliveries to construction sites were late or incomplete, underscoring the unpredictability of supply chains (source).

For retailers, a delay into the next quarter or missing the holiday season can be devastating, since the holiday period can account for a majority of annual sales for some brands (source). In short, supply chain disruptions often translate to schedule overruns (projects delivered late) and necessitate expensive workarounds or last-minute substitutions.

Mitigation Strategies for Supply Chain Disruptions

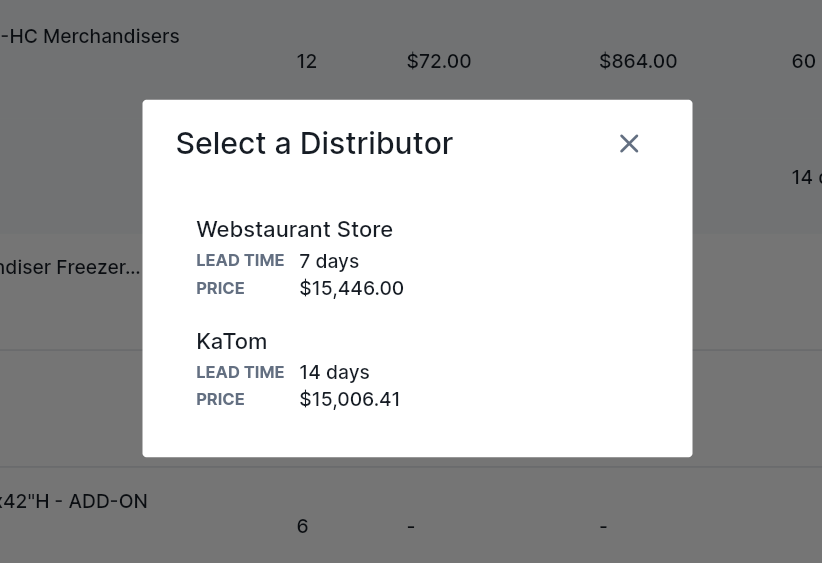

Relying on a single supplier can be a major risk—delays, price fluctuations, or inventory shortages can throw an entire project off schedule. Diversifying vendors and having backup options for critical fixtures helps retailers stay agile when supply chain disruptions arise. Real-time tracking of lead times and proactive coordination with suppliers can prevent last-minute surprises and costly delays.

Ephany makes supplier management seamless by allowing teams to compare multiple distributors for the same asset, ensuring lead times and pricing align with project requirements. For even greater accuracy, suppliers can be invited to collaborate within Ephany, updating lead times and availability directly. This keeps procurement teams working with the most up-to-date information, reducing delays and keeping projects on track—without the back-and-forth of endless emails and phone calls.

Conclusion: Keeping Track of FF&E Properly Helps Ensure a Successful Store Launch

Inefficient procurement, installation errors, and supply chain disruptions can quickly turn a well-planned retail build-out into a costly, time-consuming challenge. But with the right strategies—centralized procurement, quality-focused installation, and proactive supply chain management—retailers can stay ahead of these risks and keep projects on track.

Ephany makes this even easier by giving your team the tools to manage every aspect of FF&E with clarity and control. From tracking assets and suppliers to streamlining approvals and ensuring real-time access to critical documents, Ephany helps retailers simplify the complexities of multi-site projects—so stores open on time, on budget, and exactly as planned.

However, these aren’t the only pitfalls that can derail a retail construction project. In the next section, we’ll dive into even more budget-draining problems—cost overruns, poor project management, and damages & rework—and explore how to prevent them before they take a toll on your bottom line. Stay tuned!

It’s a thought-provoking question which reminded me of the concept of McDonaldization, a term coined by sociologist George Ritzer. This is something that I learned about in high school and it has stuck with me ever since. It describes how industries optimize for efficiency, predictability, uniformity, and control, just like McDonald’s perfected its assembly line for fast food. But this principle doesn’t just apply to burgers, it’s the secret behind how companies like Target, Walmart, and Wegmans scale their physical spaces to thousands of locations across the country.

In the world of construction and procurement, the best way to achieve this level of standardization and efficiency is through Owner-Furnished, Contractor-Installed (OFCI) items. By giving owners full control over critical assets, businesses can reduce costs, streamline procurement, and ensure consistency across every project. But what happens when projects don’t follow this approach? Chaos. Imagine if every McDonald’s location let designers pick their own furniture and kitchen equipment—it would be a logistical nightmare.

Let’s break it down.

1. Standardization & Compliance: The Secret Sauce

Just like a Big Mac tastes the same in Manila as it does in Los Angeles, physical spaces need to maintain design consistency across locations. OFCI ensures that furniture, fixtures, and equipment (FF&E) align with brand standards, regulatory requirements, and operational needs. When design teams specify their own products per project, it creates inconsistencies that make future maintenance and renovations a mess.

Imagine if McDonald’s let every franchise and/or their respective architects choose its own kitchen layout… One store might have deep fryers in the front, another in the back, and none of them would operate the same way. The same principle applies to retail spaces: consistency reduces friction and ensures every location meets the same quality standards.

In addition, each restaurant would spend countless hours selecting the kitchen equipment. This may seem like a simple trip to the appliance store, but if you’ve ever designed a commercial kitchen, you know how much work actually goes into it.

By centralizing asset decisions, owners create a repeatable, scalable playbook that maintains brand integrity and speeds up approvals.

2. Cost Savings: Cutting Out the Middleman (and the Extra Costs)

McDonald’s can sell a burger for a few bucks because it buys ingredients in bulk, cutting out inefficiencies. The same logic applies to OFCI procurement. When owners take control of purchasing, they reduce contractor markups, minimize unnecessary customization, and leverage bulk pricing across multiple locations.

A study on public works projects found that direct procurement reduces costs by up to 10% by cutting out middlemen and supplier markups (source). Now, scale that savings across hundreds or thousands of locations, and the numbers become impossible to ignore.

If every McDonald’s location sourced its own potatoes from different vendors instead of McDonald’s corporate handling it, costs would skyrocket, quality would suffer, and supply chain delays would become unavoidable. The same thing happens in retail construction when every project team sources assets independently. OFCI eliminates this waste and creates massive savings.

3. Scalability: The Assembly Line of Construction

McDonaldization isn’t just about saving money, it’s about scaling efficiently. McDonald’s doesn’t reinvent its kitchen setup for every new location; it follows a precise, repeatable formula that makes expansion fast and cost-effective. That’s exactly what OFCI does for commercial spaces.

When procurement is centralized, scaling new locations becomes a copy-paste operation instead of an unpredictable mess. Construction teams get exactly what they need, procurement timelines shrink, and store openings happen on schedule.

Compare that to a world where every project selects different assets and suppliers… It’s slow, expensive, and full of unnecessary delays. According to industry research, 80% to 90% of construction projects experience budget overruns or delays, often due to procurement inefficiencies (source). With OFCI, businesses cut through the complexity and keep projects moving.

Final Takeaway: The McDonald’s Model Works for Repeatable Design Too

The same principles that allow McDonald’s to serve billions of customers apply to construction and asset management. Standardization, cost control, and scalability create repeatable, efficient processes that drive success.

When businesses embrace OFCI, they take control of procurement, eliminate inefficiencies, and create a playbook for expansion; just like McDonald’s did for fast food. Whether you’re rolling out a hundred new stores or upgrading existing locations, this model ensures every site meets the same standards, at the lowest cost, and on time.

It’s time to stop treating asset procurement like a custom-built menu and start thinking like McDonald’s. OFCI is the key to scaling smarter.

Ephany provides a central platform to successfully manage OFCI FF&E processes. Ask me how!

Imagine your home is overflowing with clutter. You hire a professional organizer who tidies everything up—but without proper shelves and storage, the clean items just end up in a neat pile on the floor. That’s what happens when you rely solely on AI to clean up your asset data, especially when managing furniture, fixtures, and equipment (FF&E) for owner-furnished items in repeatable commercial spaces.

Here are the top three reasons why AI isn’t a magic fix—and why you need a solid platform to organize your cleaned AI data:

1. Cleaned Data Needs a Home

AI can scrub your asset data from PDFs such as drawings, product data sheets, installation manuals, and more, much like a professional organizer tidies up your kid’s playroom. But without a robust platform to house that clean data, you’re left with information floating in digital limbo.

For large-scale enterprises, relying on spreadsheets just doesn’t cut it. They simply can’t handle the complexity or scale needed to manage FF&E across thousands of locations. At a minimum you’ll want to implement a database and file repository, but then you’ll need to find someone to manage it all.

2. Context Is Everything

Imagine your kitchen when hosting a dinner party. Every tool, ingredient, and appliance has its designated spot, and everything needs to flow together perfectly. In asset management, a robust data platform works the same way—it ensures that product specifications, procurement details, maintenance histories, and other essential components all have their proper place and are connected seamlessly.

Without these relationships, or at the very least an asset identification system, your asset data is like a disorganized kitchen where the fridge, pantry, and utensils are scattered in different rooms, making it impossible to cook up efficiency.

3. Sustainable Processes Require a Strong Foundation

Imagine trying to keep your home tidy without any proper storage—no closets, shelves, or labeled bins. No matter how often you clean, the clutter just keeps coming back.

For large organizations, a consistent set of data standards is like having a custom storage system in every room. It not only keeps everything in its proper place but also enables you to automate repetitive tasks and analyze big data for strategic insights. Without that solid foundation, even the smartest AI cleanup is just a temporary fix on a constantly disorganized mess.

Introducing Ephany, an asset management platform which sparks joy.

At Ephany, we’re tackling these challenges head-on. We don’t just clean your data—we give it a home. Our solution leverages smart AI to import and polish data from PDFs (like product data sheets, installation manuals, and project details) while securely organizing it on a robust platform designed for large-scale enterprises managing FF&E for owner-furnished items. We even connect your teams to the Revit Families which include the standardized asset data that they need for projects.

By creating meaningful relationships between components, parts, and procurement details, Ephany transforms isolated data into powerful insights that drive efficiency and reduce costs.

Ready to turn your digital clutter into a well-organized powerhouse? Reach out for a free demo and discover how Ephany can streamline your asset management process.